If you are running an online marketplace that connects buyers and sellers from different countries, you probably know how important it is to enable cross-border transactions in multiple currencies.

For perspective, cross-border e-commerce constituted about 22% of global online trade in 2022 – a 6% jump from 2016. The forecast is for even more upside. According to reports by McKinsey, Statista and FedEx, global cross-border e-commerce will grow by at least 14% per year over the next four to six years.

It’s therefore a sobering reality that many of the most successful online marketplaces, such as Airbnb, Uber and Etsy, wouldn’t have had as much success if they hadn’t expanded their reach to multiple markets and currencies.

However, managing currencies in online marketplace development is not a trivial task. It involves many hurdles and risks, in particular: financial, regulatory and technical. It stands to reason that these currency-related factors can affect critical business metrics such as revenue, user experience and reputation.

In this post, we will discuss six of the most common challenges with currencies in online marketplace development and how to overcome them.

Challenge 1: Currency conversions and financial risks

One of the main challenges with currencies in online marketplace development is dealing with currency conversions. Currency conversions can occur at different stages of the payment flow, depending on your payment model and your payment service provider.

For example, if you are using a marketplace payment model, where you collect the payment from the buyer and then pay out the seller, you may have to convert the currency twice: once when you charge the buyer and once when you pay out the seller.

Currency conversions can affect your marketplace, your sellers and your buyers in various ways:

Exchange rate fluctuations can cause losses or discrepancies

Exchange rates can change rapidly and unpredictably, especially in volatile markets. This means that the amount you charge or pay out may differ from the amount you expected or agreed upon.

For example, if you charge a buyer $100 for a product that costs €80 EUR, but the exchange rate changes from 1.25 to 1.20 before you pay out the seller, you will end up paying €83.33 instead of €80, losing €3.33 in the process.

Fees and commissions increase operational costs

Most payment service providers charge a fee for currency conversions, which can vary depending on the currency pair, the amount, and the frequency of the transactions.

For example, Stripe charges a minimum 1% fee for currency conversions on top of their standard processing fees.

This means that if you charge a buyer $100 for a product that costs €80, you will pay $1 for the conversion fee plus $2.9 for the processing fee, leaving you with $96.1.

Lack of price transparency and consistency can erode user experience and trust

Buyers and sellers may not be aware of or agree with the exchange rate or the fees applied by your payment service provider. They may also see different prices for the same product or service depending on their location or currency preference. This can create confusion and distrust among your users, leading to lower conversion rates, higher refund rates and lower retention rates.

So how can you overcome these challenges?

Use a single currency for your marketplace.

One way to avoid currency conversions is to use a single currency for your marketplace, such as US dollars or Euros. This way, you can eliminate the exchange rate fluctuations and fees associated with currency conversions.

However, this solution may not be feasible for many marketplaces, as it may limit market potential and user preference. For example, if you use the US dollar as your currency, but a large number of your buyers are from Europe, they may prefer to pay in Euro or other local currencies such as Swiss Francs.

This could mean leaving a lot of money on the table. According to SaaS-focused payment solution, Paddle, pricing in multiple currencies can boost sales between 7% – 25%, depending on the number of currencies offered.

Another limitation is that many local payment options require prices to be in local currency. These include iDEAL (Netherlands), Bancontact (Belgium) and Sofort (EU and UK).

Lock in exchange rates at the time of booking or checkout

This way, you can guarantee that the amount you charge or pay out will be exactly the same as the amount you agreed upon with your users. However, this solution may not be supported by all payment service providers (PSPs), as it may require additional integrations or features.

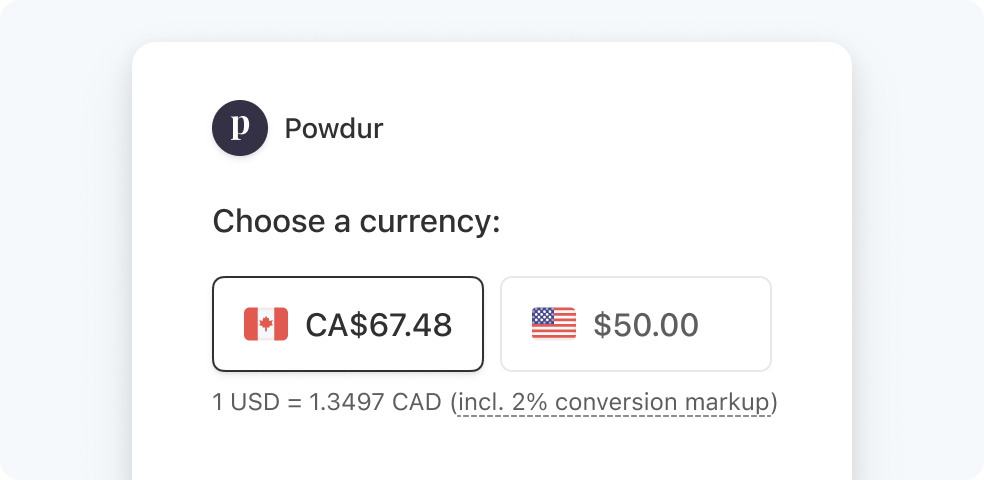

Stripe’s Automatic Currency Conversion feature allows sellers based in the US, Canada, UK and Eurozone to display prices in the local currency of buyers in 40 different countries. The exchange rate is guaranteed for the duration of the checkout session (up to 24 hours).

Drawbacks include the addition of a margin to the mid-market exchange rate, in addition to the normal card processing and currency conversion fees. The exchange rate guarantee is also subject to a 2% fluctuation threshold and doesn’t apply to subscriptions, refunds and chargebacks.

Challenge 2: Stripe currency challenges for online marketplaces

Stripe Connect is one of the most widely used payment service providers for online marketplaces, as it offers a range of features and integrations that make it easy to accept and process payments online. However, even Stripe presents some challenges when it comes to currency management.

Although Stripe supports payment in over 135 different currencies, these charges need to be converted into settlement currencies, i.e. the currency of the merchant of record. This could either be the marketplace platform or the seller depending on which Stripe Connect Charge Type is used.

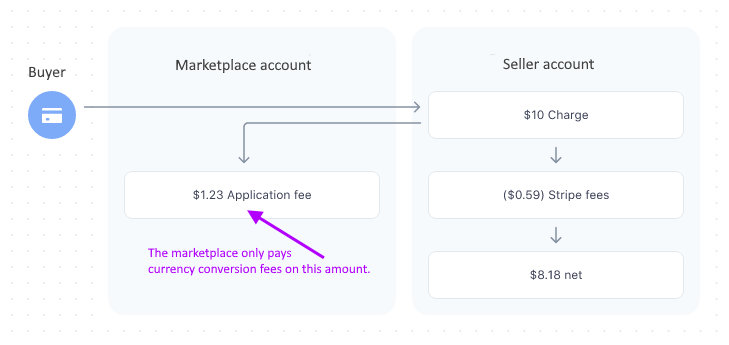

The easiest-to-implement charge type – direct charges – is a payment model where the buyer pays the seller directly, with the marketplace able to deduct a platform fee. Seller ownership of the transaction simplifies the payment flow and reduces the marketplace’s liability and compliance burden.

But most importantly, from a currency perspective, it minimises the exchange rate risks and costs, as shown in the below diagram.

However, since Stripe’s direct charge option does not support cross-border transfers, sellers can only accept card payments..

The alternative to direct charge is destination charges, a payment model where the buyer pays the marketplace, and then the marketplace pays out the seller. This way, the marketplace can handle cross-border transactions, as it can convert the currency between the buyer and the seller. However, destination charges also have some drawbacks:

- Destination charges are only supported if both your platform and the seller’s account are in the same region.

- The marketplace has to create and manage Stripe accounts for sellers. This means that the marketplace has to collect and verify the identity and bank account information of its users, which can increase its operational complexity and compliance requirements.

- It exposes the marketplace to currency conversion fees and risks. As mentioned earlier, Stripe charges a 1% (US) or 2% (non-US) fee for currency conversions on top of its standard card processing fees. This means that the marketplace has to either absorb or pass on these fees to its users, which can affect its revenue or user experience.

- Stripe does not lock in exchange rates at the time of checkout if the sellers are based in regions excluded from their Automatic Currency Conversion feature. Which means that the amount charged or paid out may differ from the amount expected or agreed upon due to exchange rate fluctuations.

- Delayed payouts and refunds have an effect on the user experience and trust. Unlike direct charge, where the seller receives the payment instantly after the buyer makes the payment, destination charge involves a delay between the time the buyer pays and the time the seller receives the payment. This delay can vary depending on the country, currency and payout schedule of the seller.

- For example, if a seller in India sells a product to a buyer in Australia using AUD as their currency, they may have to wait up to 14 days to receive their payout from Stripe. Similarly, if a buyer requests a refund for a product they bought from a seller in another country or currency, they may have to wait up to 14 days to receive their refund from Stripe.

So how can you overcome these challenges? Here are some tips or best practices to optimise Stripe’s currency management:

Use destination charge only when necessary.

If possible, try to use direct charge as your default payment model, as it offers a simpler and faster payment flow for your users. However, if you have to use destination charge for cross-border transactions, make sure you communicate clearly with your users about the fees, exchange rates and delays involved.

Set minimum thresholds for payouts and refunds.

To reduce the frequency and impact of currency conversions and fees, you can set minimum thresholds for payouts and refunds. For example, you can set a minimum threshold of $100 for payouts and $10 for refunds. This way, you can avoid paying or receiving small amounts that may incur higher fees or losses due to exchange rate fluctuations.

Choose optimal payout schedules for your sellers.

To reduce the delay and uncertainty of payouts for your sellers, you can choose optimal payout schedules for them based on their country, currency and preference. For example, you can choose daily, weekly or monthly payout schedules for your sellers depending on their cash flow needs and availability of funds.

Use dynamic pricing or currency choice for your buyers.

To improve the user experience and trust for your buyers, you can use dynamic pricing or currency choice for them based on their location or preference. Dynamic pricing is a technique that involves adjusting the price of your products or services based on various factors such as demand, supply, competition or exchange rates.

For example, you can use dynamic pricing to offer competitive prices for your products or services in different markets or currencies. Currency choice is a feature that allows your buyers to choose their preferred currency when making a payment. For example, you can use currency choice to offer multiple currency options for your products or services such as USD, EUR or GBP.

Challenge 3: PSPs have different lists of supported currencies

One of the challenges with currencies in online marketplace development is that payment service providers (PSPs) have different lists of supported currencies for sellers and buyers based on their location. This means that some sellers or buyers may not be able to use their preferred currency or payment method on your platform.

For example, PayPal supports 25 currencies for sellers and 200 currencies for buyers, but the availability of these currencies depends on the country of the seller or buyer. Stripe supports 135+ currencies for sellers and buyers, but some payment methods are only available in certain regions. Braintree supports 130+ currencies for sellers and 45+ currencies for buyers, but some features are only available in specific countries.

This can create a frustrating user experience and limit your market reach. Some users may abandon your platform or switch to a competitor if they cannot use their preferred currency or payment method.

Some possible solutions to this challenge are:

Utilise multiple PSPs to cover more currencies and payment methods.

You can integrate more than one PSP on your platform and let users choose the one that suits them best. However, this may increase the complexity and cost of your platform development and maintenance.

Offer currency choice to users.

You can let users choose their preferred currency from a list of supported currencies on your platform. However, this may require you to handle currency conversion and exchange rate risks on your end.

Use dynamic pricing to adjust prices based on currency fluctuations.

You can use a service like Currencycloud or Wise to automatically update prices on your platform based on real-time exchange rates. However, this may affect your profit margin and pricing strategy.

Challenge 4: Third-party integrations that do not support all currencies

Another challenge with currencies in online marketplace development is that some third-party integrations, such as shipping, payment methods or insurance, do not support all currencies. This means that some features or services on your platform may not work for all users or transactions:

- Shopify supports over 100 currencies for sellers and buyers, but some of its third-party integrations, such as Shopify Payments, Shopify Shipping or Shopify Capital, do not support all of them.

- WooCommerce supports over 200 currencies for sellers and buyers, but some of its extensions, such as WooCommerce Subscriptions, WooCommerce Bookings or WooCommerce Memberships, do not support all of them.

- Magento supports over 200 currencies for sellers and buyers, but some of its modules, such as Magento Shipping, Magento Payments or Magento Marketplace, do not support all of them.

This can create a poor user experience and reduce your platform functionality. Some users may not be able to access some features or services on your platform or face additional fees or delays.

Some possible solutions to this challenge are:

Using alternative integrations that support more currencies. You can look for other third-party integrations that offer similar features or services but support more currencies on your platform. However, this may require you to change your platform design and functionality.

Offering currency conversion to users. You can offer users the option to convert their currency to a supported currency before using a feature or service on your platform. However, this may require you to handle currency conversion and exchange rate risks on your end.

Using a proxy service to bridge the gap between currencies. You can use a service like Payoneer or TransferWise to act as an intermediary between users and third-party integrations that do not support all currencies. However, this may increase the transaction time and cost.

Challenge 5: Regulatory impact on online marketplace currency management

A third challenge with currencies in online marketplace development is that currency management can affect the internationalisation of online marketplaces from a regulatory point of view. This means that you may have to comply with different laws and regulations related to currency management in different countries or regions.

For example, you may have to deal with taxes, compliance, reporting or licensing issues related to currency management in different jurisdictions. Some examples are:

Taxes: You may have to collect and remit taxes in different currencies based on the location of the seller, buyer or transaction. You may also have to deal with tax implications of currency conversion or exchange rate fluctuations.

Compliance: You may have to comply with different anti-money laundering (AML), know your customer (KYC) or sanctions requirements related to currency management in different countries or regions. You may also have to comply with different data protection or privacy laws related to currency management in different jurisdictions.

Reporting: You may have to report different financial information related to currency management in different formats or standards in different countries or regions. You may also have to report different operational information related to currency management in different languages or time zones in different jurisdictions.

Licensing: You may have to obtain different licences or permits related to currency management in different countries or regions. You may also have to follow different rules or regulations related to currency management in different jurisdictions.

This can create a complex and costly regulatory environment and limit your market expansion. Some users may not be able to use your platform or face legal issues or penalties if you do not comply with the relevant laws and regulations related to currency management.

Some possible solutions to this challenge are:

Using a local entity to handle currency management in different jurisdictions. You can set up a local subsidiary or partner with a local company to handle currency management in different countries or regions. However, this may require you to invest more resources and time in your platform internationalisation.

Outsourcing compliance to a third-party service provider. You can use a service like Stripe Atlas, Shopify Global Ecommerce or Amazon Global Selling to handle compliance related to currency management in different jurisdictions. However, this may reduce your control and visibility over your platform operations.

Following best practices and standards for currency management. You can follow the best practices and standards for currency management recommended by industry associations or organisations, such as the International Organization for Standardization (ISO), the World Wide Web Consortium (W3C) or the International Monetary Fund (IMF). However, this may not cover all the specific requirements or nuances of different jurisdictions.

Seeking expert advice on currency management. You can consult with experts on currency management, such as lawyers, accountants, consultants or advisors, to help you navigate the regulatory landscape related to currency management in different jurisdictions. However, this may increase your operational cost and dependency.

Challenge 6: Seller payouts and financial risk mitigation

A fourth challenge with currencies in online marketplace development is that currency management can impact seller payouts and what are the financial risks involved. This means that you may have to deal with different issues or challenges related to seller payouts in different currencies.

For example, you may have to deal with exchange rate fluctuations, fees or delays related to seller payouts in different currencies. Some examples are:

Exchange rate fluctuations: You may have to deal with the risk of losing money or profit due to changes in exchange rates between the time of the transaction and the time of the payout. You may also have to deal with the risk of upsetting sellers or buyers due to changes in prices or earnings due to exchange rate fluctuations.

Fees: You may have to deal with the cost of paying fees for currency conversion, transfer or processing related to seller payouts in different currencies. You may also have to deal with the cost of passing on these fees to sellers or buyers or absorbing them yourself.

Delays: You may have to deal with the time of waiting for seller payouts in different currencies to be processed, transferred or cleared by different parties involved, such as PSPs, banks or intermediaries. You may also have to deal with the time of resolving any issues or disputes related to seller payouts in different currencies.

This can create a negative user experience and affect your platform performance. Some users may not be satisfied with your platform or switch to a competitor if they do not receive their payouts on time, in full or in their preferred currency.

Some possible solutions to this challenge are:

Using conditional payouts to reduce exchange rate risk. You can use a service like Currencycloud or Wise to lock in exchange rates at the time of the transaction and pay out sellers at a later date based on these rates. However, this may require you to pre-fund your payout account and trust the service provider.

Using batch payouts to reduce fees and delays. You can use a service like Payoneer or TransferWise to pay out multiple sellers in multiple currencies at once using a single transaction. However, this may require you to align your payout schedule and frequency with the service provider.

Using hedging strategies to mitigate financial risk. You can use various hedging strategies, such as forward contracts, options or swaps, to protect yourself from adverse movements in exchange rates related to seller payouts in different currencies. However, this may require you to have financial expertise and access to financial markets.

Offering product prices in the local currency of buyers and paying out sellers in their chosen currency can have a huge impact on their user experience and therefore your marketplace’s profitability.

The complexity of implementing and managing the various aspects of cross-border transactions may present a significant challenge, but this could also be a powerful competitive advantage for your online marketplace. There’s a reason why no-code marketplace builders like Sharetribe don’t offer currency support out of the box.